Bank Runs and the Public Markets

Last week, as First Republic Bank headed toward the dustbin of history, I wrote this in Substack Notes:

Would First Republic eventually have suffered depositor outflows and financial weakness sufficient to prompt an FDIC takeover, even without their terrible late-April earnings call? Maybe. Would it have happened last week? I suspect not.

Then this week happened, and it got even weirder: stock prices of PacWest Bancorp (which owns Beverly Hills-based Pacific Western Bank) and Western Alliance Bancorporation plummeted, then somewhat recovered. Yet, those banks had said deposits stabilized in April after the March outflows sparked by Silicon Valley Bank’s failure. Their recent earnings calls had gone well.

By Wednesday evening, Reuters reported that PacWest was engaged in “strategic options talks”—and on Thursday, Western Alliance denied a false rumor that it was exploring a sale, calling the rumor “shameful.”

So, what’s going on with the stock prices?

It’s starting to look like, in the current environment, stock price freefalls can sometimes increase existential risk for banks, if not cause it to fully manifest. (Yes, I know Matt Levine just sent out a newsletter about this, which you should read. What I’m writing about here is some variant on his Possibility 4—a theory that short-sellers are attacking regional banks deliberately—though I think their motivation is simply to make money, not because they have any particular wish for banks to fail. They made a lot of money on PacWest and Western Alliance this week, even if those stocks ultimately end up recovering.)

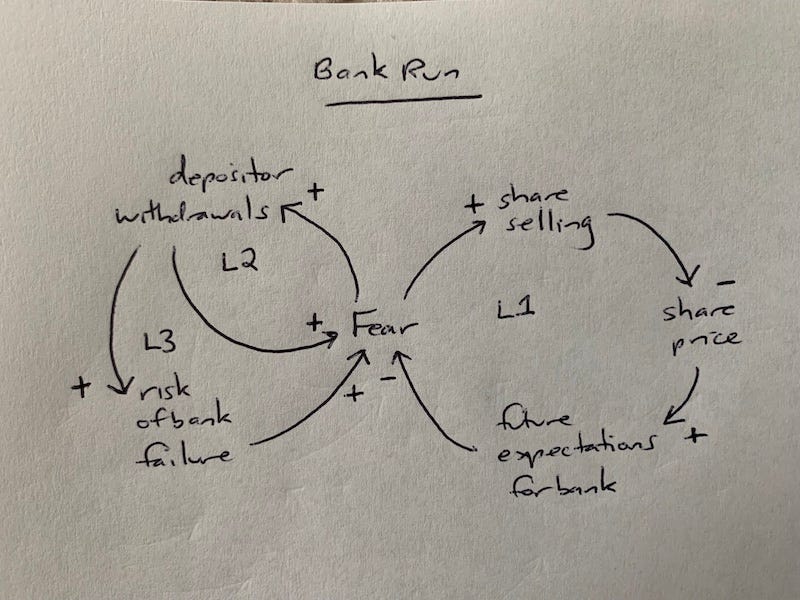

So, how does this work? A few weeks ago, I wrote an essay on the system dynamics of bank runs. Here’s the simplified version of a causal loop diagram from that essay for a publicly traded bank:

I said in that essay, and still believe, that being publicly traded might increase the likelihood of a bank run. With more eyes on financial statements (both long investors and short-sellers), there are more people who might tweet or call out hypothesized or actual weaknesses. And if short-sellers perceive a profit opportunity and cause a stock selloff, that can affect future expectations for a bank by generating negative headlines.

There are probably privately traded banks with duration mismatch challenges, but without quarterly earnings calls and a public stock price, their depositors are much less likely to look at the news and go, “Why is my bank in the news? Why is the stock price falling? Uh-oh, is my money safe?”

A thought experiment on going private

So, why do small and regional banks go public in the first place? I’d argue they probably shouldn’t, and that going public probably exposes them to greater existential risk compared to staying private. Going public might be better for managers at the bank (at least during the initial IPO payoff) but is likely not so good for the company, at least not in today’s environment of social media contagion and 24-hour, fast-twitch high-hype news cycles.

Which brings me to a radical idea I mused on in Substack Notes earlier this week:

Of course, I think it’s unlikely regulators could or would take small and regional banks private en masse (and just one or a few banks announcing a go-private strategy could find themselves targeted by short-sellers, which would be counterproductive). But it would be interesting to model or simulate what might happen in a broad go-private scenario.

What about transparency?

One thing that wouldn’t suffer much if more banks were privately traded is transparency. That’s because FDIC-insured banks’ financial data is published quarterly in the Uniform Bank Performance Report, which is publicly available. This report includes an income statement, a balance sheet, and lots of other financial data at detailed and summary levels. This marks a difference between banks and other types of businesses: whether public or private, their financials are available.

There are other ways that banks have different dynamics than other types of businesses. For example, loss of bank customers (depositors) can lead to loss of even more customers—to an outsize degree. As I wrote in one of my Substack Notes: “Hypothetically, if Costco had a bad quarter and lost a lot of members, it’s unlikely the rest of its members would flee en masse toward BJ’s and Sam’s Club.” But that’s basically what can happen to banks.

And hypothetically, if Costco’s stock price were to fall, it’s unlikely that its members would think much of that at all. It would have very little bearing on the $1.50 hot dog or a pallet of toilet paper. Banks are different because they are safekeeping their customers’ money. And maybe it’s time to think about them a little differently in the context of markets.

I am not a finance person but read a lot, especially non-fiction history. When I look at the history of the United States, ESPECIALLY the emergence of Investment banking (Civil War) has brought with it a remarkably unstable banking system with runs on banks built in. The worst of the worst always emerge whole. It seems to me that the MOST IMPORTANT element of banking failures should be punitive to ensure taxpayers are not getting fleeced. I think bank failure should be treated as a red badge and officers and key employees should be banned from both banking and regulating for perhaps 10 years and even lifetime on the second occurrence. I especially observe the seeming absence of this foolishness in Canada and frankly lots of countries. This remarkable distortion which rewards WRECKLESS risk-taking is the fuel to better returns (insulated from the downside risk by so-called regulators). These investments with higher returns fuel inequality among their other failings.

Finally, liquidity standards should be sacrosanct and reportable CONTINUOUSLY, not just quarterly. This should be the tax associated with government insurance. I would actually prefer performance bonding and not just a balance sheet. Performance bonding can survive bankruptcy and reorganization and can even be attached to officer holdings.