Consequence-Weighted ROI - A First Step

ROI is a finance acronym for return on investment. For example: if I invest $1000 in something, how profitable will that investment ultimately be? ROI is often expressed in terms of today’s dollars using a net present value (NPV) calculation. NPV is a valuation method that discounts future cash flows back to the present. That essentially means it values the future lower than the present.

Here’s an example of NPV in action: you invest $10000 in a startup that you anticipate will produce a $100000 payout to you five years from now (for example, you think the startup will get acquired). In year 0 (today), your outlay is $10000 in today’s dollars. But if the “discount rate” (aka the rate at which money depreciates) is 5%, then five years from now, the NPV (amount in today’s dollars) of your payout will be less than $100000, according to this formula:

C / (1 + r)^n

where:

C = cash flow

r = discount rate (.05 in this case)

n = period (year in this case)

Here’s the calculation of your expected payout at the end of year five:

100000 / (1.05)^5 = 783531

You’re not going to get $100000 in today’s dollars. But in pure mathematical terms, you should still make the investment, because $78353 is more than your $10000 initial investment, which means an expected profit of $68353 in today’s dollars ($78353 minus your initial outlay of $10000). Unless you can get a better return on your $10000 elsewhere, you should invest in the startup (if it’s within your risk appetite2)!

What does this mean for risk management?

A few things. For risk management investments, the question is often a little different: If I spend $1000 on a mitigation measure, how much loss will I probably prevent, and will the loss prevented outweigh the expense? This can be a harder sell when pitching investments to senior management, since loss prevention can be hard to quantify.

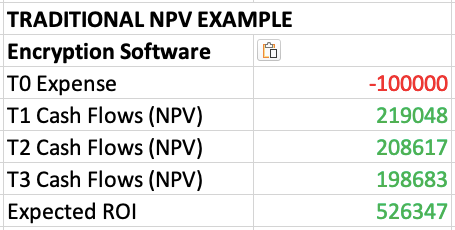

Encryption software to prevent data loss or theft, for example, may cost $100000 in direct software costs and labor costs up-front, plus $20000 per year for maintenance and support. It’s probably not going to earn your company anything. Ouch. But if the software prevents five data loss incidents per year, and each incident costs on average $50000, suddenly it starts to look like a great investment, if you can accurately quantify the expected savings and convince senior management.

Here’s the calculation over a three-year time horizon:

-100000 / (1.05)^0 + (250000 - 20000) / (1.05)^1 + (250000 - 20000) / (1.05)^2

+ (250000 - 20000) / (1.05)^3= -100000 + 219048 + 208617 + 198683

= $526347

Now, consider what happens to the math if a massive theft of unencrypted personally identifiable information (PII) in a jurisdiction with strict privacy laws would cost $20 million in fines, plus additional costs related to offering consumer credit monitoring services, legal expenses, and reputational damage. That encryption software looks even more amazing, even if the catastrophic incident occurs only once per decade.

So, NPV seems pretty great even for risk investments.

Yeah. But NPV has an interesting effect at distant time horizons. Let’s say that massive $20 million PII theft occurs at the end of year 30. What’s the NPV of the loss?

20,000,000 / (1.05)^30 = $4,627,487

Let’s say it occurs at the end of year 80:

20,000,000 / (1.05)^80 = $403551

The impact is less than 1/20th the size in today’s dollars. This is more of a thought experiment when debating the purchase of encryption software with a positive NPV even in year 1—but it’s a huge problem when considering massively expensive present-day investments to mitigate impacts of climate change that won’t materialize for decades.

NPV just falls apart for this use case.

Time for another example?

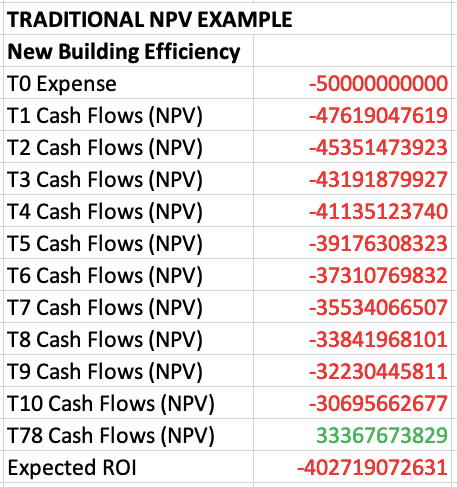

Sure. Let’s say it will cost an extra $50 billion per year for the next 10 years to construct all new buildings to more efficient standards.3 If we do it, warming should decrease by about 0.3 degrees Celsius by the year 2100, which will save $1.5 trillion (and countless lives, which are more important and often glossed over by these types of calculations and that's a whole other issue).

But look what happens to our anticipated savings when we apply a traditional NPV formula (I’m not going to write out all the math because it’s the same approach used in the encryption software example earlier):

The $1.5 trillion in savings, 78 years from now in 2100, is worth only $33.37 billion in present-day dollars.4 That’s less than Elon Musk paid for Twitter! It’s not nearly enough to overcome the nearer-term costs of $50 billion per year.

Sometimes governments make investments that aren’t ROI-positive, but with climate change, companies need to get on board too. And no rational company will take this deal purely on financial merits.

But climate change is going to disrupt everything.

True. And that changes—or should change—the calculation. Many climate investments just don’t pass the NPV bar, and we need to make them anyway to save lives, economies, and societies. Sometimes, we even need to choose them over NPV-positive investments with more near-term benefits. But how do we formalize a method for prioritizing investments that prevent or mitigate unacceptable consequences, since the consequences are too far in the future to move the NPV needle much?

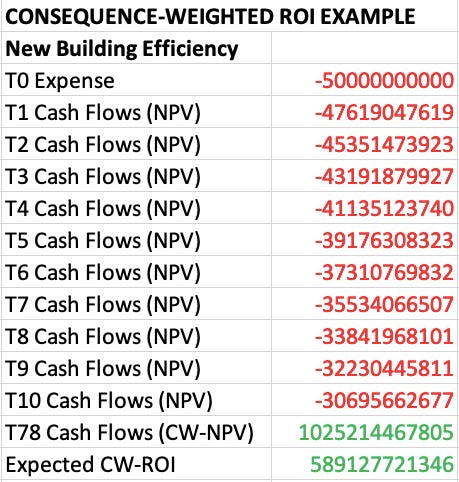

One answer is that we can alter our NPV equation to weight unacceptable consequences—and the savings from preventing them—more heavily. For example, we might agree that increased warming of 0.3 degrees Celsius—the consequence of not making the new-building efficiency investment in our example—is unacceptable. I’d argue we should deem it unacceptable, since a recent study on climate tipping points shows we may have already passed the threshold for five of them, and more are close on the horizon. Importantly, wherever the threshold of “unacceptable” is set, it should be clearly stated so results are consistent and replicable by different parties.

For purposes of this example, we’ll apply a weighting to our massive future savings from new building efficiency. We’ll introduce weighting factor W, which will be multiplied by time period t, and we’ll use our consequence-weighted equation to calculate the far-future benefits of the investment:

C / (1+r)^(t*W)

I’m going to set W equal to 0.1, applying a 10x weighting since the outcome without this investment is unacceptable. Note: there is no standard for consequence-weighted ROI yet, so a different weighting might turn out to be more optimal.5 Whatever the agreed-upon value of W, it should remain constant for all investments that are made to prevent or mitigate unacceptable risks. An agreed-upon standard would allow consistent comparison of different must-do investments and prioritization of the ones with the greatest expected ROI.

So let’s do this consequence-weighted calculation of the savings realized by averting an unacceptable outcome:

1,500,000,000,000 / (1.05)^(78*.1) = $1,025,214,467,805

Here’s the spreadsheet version of the calculation incorporating consequence-weighted ROI:

That’s $1.025 trillion saved in exchange for our investment of $50 billion per year for ten years. Our consequence-weighted NPV calculation is now positive, because we brought the benefit of the investment forward in time, since without the investment, an unacceptable outcome will occur.

What’s the takeaway?

W is basically a factor of how much we care about preventing unacceptable outcomes in the future. Traditional NPV calculations say, “Not much.” But it increasingly looks like that answer is wrong. Climate change advocates routinely talk about the effects that changes made now or soon will have by the year 2100. And consequence-weighted NPV might be a good way to better account for and emphasize two things:

The cost of catastrophe in the far future.

The savings realized when catastrophe is averted in the far future.

Both of those things tend to vanish in the mists of traditional NPV calculations. But if the distant catastrophe we aim to avert with an investment today is unacceptable, and the distant savings we realize from averting that catastrophe are massively meaningful and consequential, then we need a better tool.

Let’s consider adding consequence-weighted ROI to the toolbox.

Note: This is just a first-step thought experiment. I’ll be reaching out to economist friends and professors to seek feedback and refine this idea, and I welcome your thoughts. Please send me a note at riskmusings@substack.

As a side note, this is one reason why a fixed-rate mortgage can be a great deal: you pay less and less over time, on an inflation-adjusted basis.

Maybe you don’t have enough spare cash to tie up your funds in an illiquid investment for five years. Or maybe your expected payout is calculated based on a 20% chance the startup is acquired by the end of year five, and you can’t handle the 80% chance that your invested money remains illiquid if an acquisition doesn’t happen. Those would be good reasons not to make the investment, and to accept a lower ROI in a more liquid investment.

Leave aside, for the moment, the complex reality that many companies are involved in building new buildings, so the ROI calculation wouldn’t really be based on one giant pot of investment and one giant benefit in the future. Also, these numbers are made up for purposes of this example.

All right, here’s the math: 1,500,000,000,000 / (1.05)^78 = $33,367,673,829

For example, W could be set to .2 for a 5x weighting, or .0667 for a 15x weighting, and so on.

Kudos Stephanie. I believe writing that touches on mathematics is one of the most difficult of all topics yet yours was the right mix of useful and descriptive. My favorite current example of system thinking is preparation for the non-zero chance of an asteroid impact. We have very limited data, we know it is catastrophic and it might likely end virtually all life on the land masses of the planet. Against that risk, it is very hard to figure out how much to spend on mitigation.